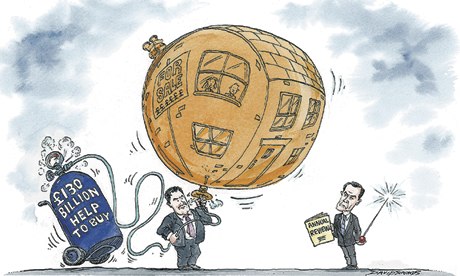

The Bank of England governor now has a veto over the inflationary Help to Buy scheme. The question now is whether he will dare to slow the housing market as 2015 looms closer

When Mark Carney succumbed to George Osborne's overtures (plus a very large cheque) and brought rock-star central banking to Britain, he probably didn't imagine that, just as he was honing the Bank of England's new tools for taming asset bubbles, the chancellor would be deliberately pumping up a housing boom.

We may never know whether Carney called the chancellor and demanded the power to call time on his controversial Help to Buy scheme; but Osborne's decision to give the bank an annual veto was a significant climbdown – perhaps not on the scale of the pasty tax, or any of the various other elements of the 2012 budget that were subsequently chopped, but humiliating nonetheless.

The centrepiece of this year's budget, Help to Buy was a political masterstroke, pumping up public confidence just as many potential buyers were thinking about returning to the estate agent and helping the government claim credit for an upswing in the property market that had already been kicked off by the Funding for Lending Scheme.

Economically, however, Help to Buy is madness, as the Treasury select committee, the IMF and outgoing governor of the Bank of England all lined up to say.

Offering taxpayer subsidies for high loan-to-value mortgages, just as the boom-bust British housing market is moving from stop to go, is at best risky, at worst reckless – and with every week bringing fresh evidence that the property bounce is spreading far beyond the capital, it looks more dangerous by the day. Even estate agents – as represented by the Royal Institution of Chartered Surveyors – have called on the bank to impose a 5% cap on house price inflation.

Initially, the Treasury's argument was that the scheme would help spark a building boom, as the surge in demand prompted developers to restart long-stalled projects. Housebuilding has picked up modestly, but by common consent it remains well below the levels required to keep prices stable.

Meanwhile, the body left with the difficult and controversial task of pricking a future housing bubble is the new, untested financial policy committee (FPC) within the Bank of England. Before the committee has found its feet – and the public have even noticed it exists – it is being forced to contend with a government-backed scheme aimed at bringing forward up to £130bn in mortgage lending to risky borrowers who are not served by the banks. Most recently, the Treasury's justification has switched from giving developers an incentive to the narrower rationale of fixing a specific "market failure" for borrowers with small deposits who struggle to get mortgages. But whatever the explanation of the moment, before Friday's cave-in, Carney faced spending the next year fielding relentless questions about a housing bubble at the same time as the Treasury was pumping out loans.

Even now, the FPC will only be allowed to pronounce on the scheme after 12 months; but that must be better than maintaining the pretence that subsidising homebuyers is a purely political matter, to be left to the Treasury, while forestalling a crash can be left to the number-crunching technocrats in Threadneedle Street.

Treasury officials were keen to deny that the move signalled any concern on Osborne's part that his pet scheme could be risky – heaven forfend. But it wouldn't be at all surprising if Carney, hand-picked by the chancellor to drag the economy out of the doldrums, had demanded the power to pull the plug on a pre-election wheeze that could cost the economy dearly. Whether he'll have the guts to do so next September, just eight months before the election, is another matter. Now that really would be independent central banking.

Livingston gets massive BT payout in under the wire

When he resigned from BT to become trade minister in the coalition government in June, Ian Livingston admitted he had been "well rewarded" during his decade at the telecoms company. He could afford to take the unpaid job. "I'm clearly not in it for the money," he said of his new post. "It's a fascinating role and I can make a difference. I have been well rewarded over the years at companies where they've done well."

When he made those remarks the company's annual report showed he had received a £925,000 salary, a cash bonus of £1.2m and another £270,000 to pop into his pension. It also provided details of bonus schemes releasing shares worth almost £10.5m that dated back a number of years. Since then, another share-based deferred bonus plan worth £3.4m has been released to him, and stock exchange disclosures show Livingston sold every one of those shares on 30 July.

Even so, BT's remuneration committee – chaired by former Labour minister Patricia Hewitt – has now handed him shares worth almost £9m (justifying that largesse by pointing out that Livingston was leaving behind other, so far unearned, bonuses worth a similar sum.)

The City was thrilled by his performance at BT – the share price rose from 75p around the time he took the helm in 2008 to the 12-year highs above 342p at which it currently trades – so investors may be willing to turn a blind eye to this generous gesture

when BT's executive pay arrangements go to a vote next July. Nonetheless, shareholders will rightfully wonder whether the principles cited by remuneration committees for big pay awards – to attract, recruit and retain top bosses – apply in this case. And the payout might just have a bearing at the government department he is joining: the department for business, innovation and skills.

That's the one that reckons it can clamp down on boardroom pay – and is bringing in new rules next week in a bid to do exactly that.

Tell Sid – we've no idea what Royal Mail is worth

What is the Royal Mail worth? Who knows – maybe £2.6bn, maybe nearly 30% more. That's as good as the estimate gets, even though investors are now being asked to buy shares in a privatisation that even Margaret Thatcher decided was best worth avoiding.

The eventual price will be set by big City institutions placing offers for shares which will be priced between 260p and 330p, thus valuing Royal Mail between £2.6bn and £3.3bn. It leaves the small investors – the new generation of Thatcher's Sids – who might be considering buying shares in the uncomfortable position of having no real idea of what they will have to pay.

The minimum subscription of £750 could leave a retail investor with 288 shares if they are priced at the bottom of the range and 227 at the top. The dividend – which will be attractive to income investors – will be somewhere between just over 6% and just under 8%.

Surely there must be a better way, in the 21st century, to organise a sell-off.

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment